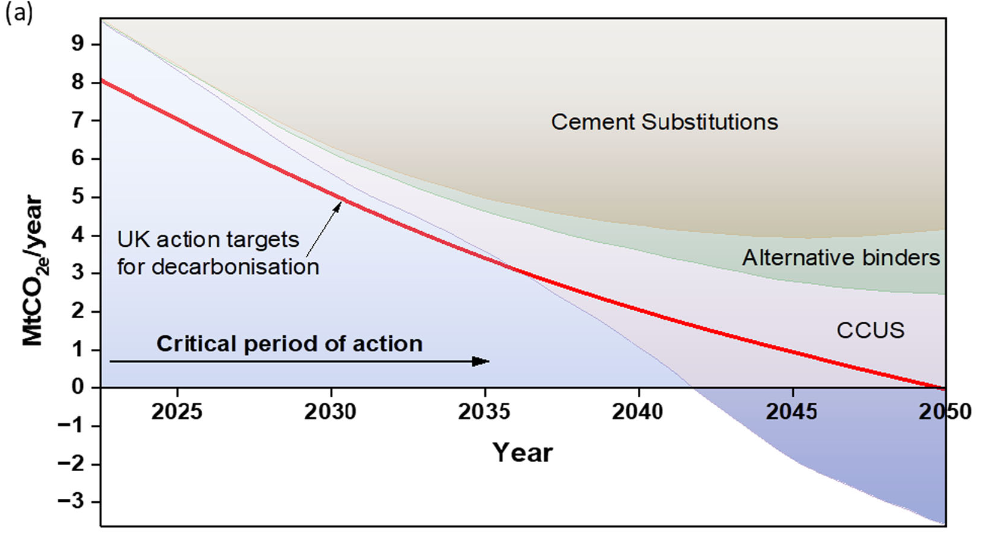

Li, N., Unluer, C. Towards a net zero built environment: decarbonisation of the UK cement industry. npj Mater. Sustain. 3, 10 (2025). https://doi.org/10.1038/s44296-025-00052-0. Fig. 6 | Decarbonisation of the UK cement industry. a Technology decarbonisation roadmap.

Decarbonising the cement industry is a global issue that is intensely local. Cement (and concrete) are responsible for between 7% and 8% of worldwide CO2 emissions, just 1.5% of emissions in the UK, but around 25% in Staffordshire Moorlands and High Peak. The exceptionally high local figures reflect the concentration of the industry in the district; the relatively low UK figures partly reflect our increasing reliance on imports, some from countries with no decarbonisation plans in place.

The path to emission reduction chosen by the UK government and the industry involves increasing carbon taxes, partially subsidising the industry’s investment in carbon capture, usage and storage (CCUS), while protecting it from ‘dirty’ imports via the European Carbon Adjustment Mechanism.

It is often overlooked that even the government and the cement industry accept that CCUS technology can only be part of the solution and that alternative products and better construction practices play as important a role in the path to Net Zero. That said, many people argue that the cement industry needs to transform itself more fundamentally instead of using expensive CCUS technology to continue ‘business as usual’.

There certainly are potential alternatives to Ordinary Portland Cement (OPC) and this article provides links to some of them. There is no doubt that CCUS does lessen the pressure on the cement industry to investigate other, low-carbon products. But retooling a whole industry as well as much of the construction trade involves far deeper issues than technological breakthroughs, in particular:

- Can novel cement production be scaled up in the timescale needed to meet climate targets?

- How to address issues of potential raw material scarcity for some of the most promising alternatives?

- Could the range of different products meet building industry standards (in a regulatory environment already much more cautious as a result of experiences such as Grenfell and failing school structures)?

- How feasible is it to retrain a construction trade already under severe stress?

- What do you do about lime production (from the same plants ascement and a key ingredient in many commercial and domestic products)?

- What are the economic, social and carbon costs of scrapping one whole industry to replace it with another?

Putting all these pieces of a jigsaw together to come up with a definitive answer is beyond us, and as far as we can ascertain, no-one has yet managed it. But in an attempt to provide people with some routes into the issues, and allow them to make up their own minds, here is a selection of some of the more recent ones.

A quick read though with good links from The Conversation Website.

A well-written introduction on the race to decarbonise concrete at scale, with good links, from the Centre for Construction Best Practice.

An exceptionally useful paper published in Nature (npj Materials Sustainability) which includes a roadmap to industry decarbonisation based on deployment of all available technologies.

An academic paper from The Journal of Sustainable Production and Consumption which strives to measure both the likelihood and effects of different routes to decarbonisation in the UK

A dauntingly wide synthesis of literature on the issues facing decarbonisation in the global cement industry from the Journal of Environmental Management.

A very readable introduction to some companies that are making alternatives to traditional Portland Cement

A very brief introduction to some of the alternatives from University of the Built Environment.

One alternative that is already being used in major UK infrastructure projects.

An article from Physics World that highlights some of the cutting edge research in new additives.

At least one company in the US has managed to produce cement that meets regulatory building standards in that country.

The roadmap for the lime products sector from industry organisation the Mineral Producers Association.

Swiss company Holcom is the owner of the Cauldon plant and this is their sustainable construction brochure.

This report from trade body UK Concrete contains a useful map of where plants are located in the UK.

A paper from the Institute of Civil Engineers which analyses how improving construction practice can reduce lifetime carbon costs.

And this explainer from the same source is a very clear read.

A 2022 Parliamentary Report on whole life carbon in construction.

This opinion piece uses the example of reinforced autoclaved aerated concrete (RAAC) to warn of the perils of new building materials that work well in the laboratory but may not stand the test of time.

Any number of reports highlight how the UK building industry effectively needs to rebuild itself in order to have the numbers of workers available with skills necessary to meet Net Zero targets.

A 2022 Parliamentary Report on whole life carbon in construction.

And finally, a recent Parliamentary Question on the decarbonisation of cement from the MP for Derbyshire Dales.